Platforms and Negotiation Leverage

The 3rd in a 4 part series on platforms as a business model in logistics.

This is the third in a series of articles on platforms as a business model for the logistics sector. It connects with a three hour podcast in which I discussed the same topic with my friend Märten Veskimäe. Check out the podcast at Logistics Tribe on Apple or Spotify. If you like this kind of analysis, sign-up to the newsletter.

Ben Thompson as the Aggregator OG

If you are discussing platform strategy often at all, eventually someone will mention aggregators in the same way we might hint to a friend they have something in their teeth. There follows a painful introspection, part of which is going to be reproduced here. An important hallmark of this process is to spend about half the time you have available trying to define these two business models. Then we can decide when to pursue one over the other.

By far the most writing on this topic is by Ben Thompson. I added footnote links for the articles I found the most compelling, but I cannot even be sure I've caught all his articles, posts, and podcasts on the theme. Hat-tip to him for both his original thoughts and the collection of previous thinking on platforms vs. aggregators. Ben's focus is purely on the consumer markets, so he draws on examples like Microsoft, Uber, Bird, Etsy, 1stDibs, LinkedIn, Google, Apple, and so forth. I'm going to end up mostly contrarian to Ben but will do the longform thinking to get us there. He never said it this way, but I believe Ben's five main hypotheses on platforms vs. aggregators goes as follows:

The value chain for any given market is divided into three parts: suppliers, distributors, and consumers.

The internet age converted previously foundational value chain activities from incremental cost to zero-incremental-cost. For example: infinite shelf space for inventory of e-commerce. This enables both aggregators and platforms. This shifted the balance towards distributors competing on scale of supply or consumer base.

While both models achieve supply-demand match, platforms establish means for counterparties to interact while aggregators instead capture one side and become their representative to the counterparty via intermediation. Example: Uber aggregates drivers and the rider buys transport from Uber not from the driver.

[Following the view of Bill Gates]: Platforms produce more value for the ecosystem than they extract for themselves, while aggregators extract more than they leave for their participants.

In a market where suppliers can be commoditized, the hard side for matching is the consumer. Aggregator business models will win, and in turn extract more value. And vice-versa: differentiated suppliers will avoid aggregators.

Nope. It’s Just Leverage.

Ben's points above (which, again, he makes more verbosely, and I tried to compress) seem valid per se. But I think they miss the right level of abstraction for two reasons. First, he only considered consumer businesses and therefore makes a whole theory for a sub-set of platforms, when in fact there is a more satisfying general theory of platforms. Second, he's calling out outcomes not inputs when talking about depth of intermediation, commoditized suppliers, and technology enabled zero-incremental scaling costs.

So here is my take on platform vs. aggregation in three hypotheses:

Platforms are intermediary businesses: they enable interactions of counterparties (i.e., the platform members).

Those members have different levels of leverage in their value chain, sometimes altered by the arrival of the intermediary. Leverage here can be thought of like negotiation leverage: it comes from their BATNA.

The optimum (or even viable) platform will manifest the leverage the members. In some cases, the leverage means no viable platform is possible or desirable.

So, let's unpack this abstraction…. The first claim is straightforward: platforms need “sides” on them, i.e., the counterparties to whatever interaction the platform helps make possible. Tinder doesn't date you: it helps the boys and the girls find each other (or whatever sexual orientation permutation you want to use).

The second hypothesis is where the fun starts. When I read Ben Thompson, I think he dances past the blindingly obvious fact that platform members will have negotiating leverage in their value chain. This is where a general theory of platforms starts to make more sense than Ben's consumer-focused one. Anyone working in B2B knows the asymmetry of leverage in value chains. I wrote in 2010 about how supply chains almost always end up coordinated by a strong anchor member rather than via federation of equally strong member companies. Twelve years later this is even more common. What Ben's focus on consumers does is to treat the demand side of the value chain as a given: a vast pool of anonymous demand in which only desires and user experience are considered, and no agent-principal conflicts can occur. That's not going to work for B2B platforms, but perhaps more importantly it won't always be true of consumers either. Technology, regulation, economic conditions, or demographics may warp how much leverage consumers have the in the value chains their anchor. By skipping them as an object of assessment, Ben's model may not even work for all B2C platforms.

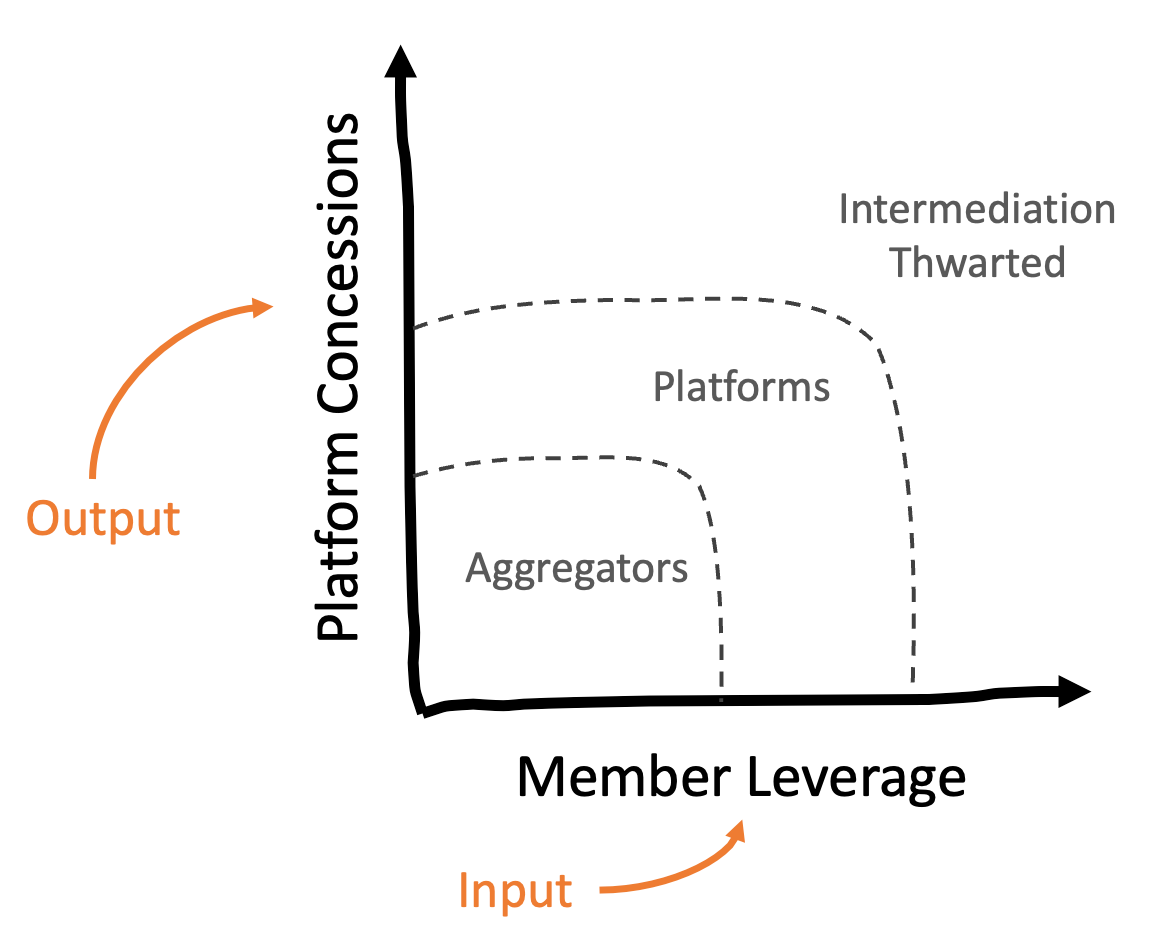

The third hypothesis is where I assert a simpler explanation for the platform-aggregation dichotomy. Business models tied to intermediation will need to be accepted by the counterparties they intermediate: no one can simply force intermediation on existing markets. Although intermediation tends to alter the leverage of the existing players, there will still be variations in who has the power even post-intermediation. Owing to that leverage, to the extent that a platform's success or failure can be determined by one of its members, then that member's interests will be imposed in the resulting business model. Finally, this brings us to the crux: at the extremes of resulting leverage (post-intermediation) you have non-platforms, while in the middle you have platforms of various degrees of concessions to keep members onboard.

The image above suggests there are three zones for an intermediating business:

Let's call the first possibility “aggregators” to justify the fact we spend so much time on definitions. The hallmark is that the intermediator becomes a counterparty, de jure or de facto. These business models emerge when intermediation results in extreme weakness of one group of members. Because the group is so weak, the intermediating business does not have to give them concessions in the business model. The result is an intermediating business that is too directly involved and strong to make sense as a platform (where some degree of neutrality is expected). A handy example that comes to mind is Uber in ride hailing. You'd be hard pressed to say they aren't simply in the value chain as the counterparty instead of a platform helping riders and drivers find each other. Bottom line: weak members as an input means platforms just become value chain members and direct counterparties. This also leads to seizing more value as the intermediary, since doing so is possible and desirable.

The second possibility is that the intermediary is facing counterparties with enough leverage to command some concessions on how the business model works. A site like YouTube faces powerful members on all three sides (consumers, content creators, and advertisers). I'll talk more below about how these dynamics play out, especially in logistics (since that's ultimately what I'm focused on). But for now, let's just say that with limited leverage I think members tolerate platforms as a viable intermediary model, and would essentially block the arrival of aggregators who attempt to act as the counterparty.

The third possibility (and frankly the default in B2B) is that the intermediation fails because some segments of the required counterparties are powerful and can veto its arrival. Sometimes they'd block an intermediary instinctively, or out of inertia. But often it’s because everyone at the dinner must eat, and an intermediary's value just doesn't seem worth keeping them fed. As an example: discount airlines like Ryanair or EasyJet blocked flight searching websites.

The Goldilocks Zone Theory of Platforms

As said above, I think there is a viable space for intermediation by a platform when the members have some leverage, neither too little nor too much. But the zone is large enough that specific mechanics will emerge to reflect these power dynamics. Or, put another way, successful platforms optimize for member leverage differentials. I think this manifests in the choices platforms make in the following dimensions (among others, since this isn't exhaustive):

The standards definition (what data can be shared; what actions can be taken)

The depth of intermediation (i.e., catalogue, search, recommend, or assignment)

Whether intermediation occurs in payments or not

Pricing model for the platform (what's free, what's charged, how is the charging metered, etc.)

Arbitration power for disputes

So, for example, a platform like LinkedIn is a platform for three member groups: professionals, navigators, and advertisers. Professionals seem to me to have the most leverage. Even if a small (but highly sought after) group were to abandon LinkedIn, this would endanger the platform health. That leverage manifests itself in decisions like the free-to-use commercial model, the fact that we can find each other by name search (rather than just recommends, or email lookup, for example), and dispute resolution that errors on the side of not bothering the professionals. Navigators (i.e., recruiters or salespeople who are looking for leads) have less leverage. A much larger number of them must leave before platform health declines. So, the platform optimizes a bit further away from their interests: this group pays for access, they are rate limited in the number of new contacts they can make, and they can be throttled further if they are seen as bothering the professionals. What we see here is that an optimal platform is making specific design choices about its mechanics and business model based on the leverage or power of those it’s trying to intermediate. Ignoring these factors results in worse platform adoption, lower value extraction for the platform operator, and risk of an alternative platform that better reflects the situation on the ground.

Let's Talk Logistics

The aggregator vs. platform question seems simpler to me in logistics than in other domains. Logistics has had 3PLs (also called forwarders, also called brokers) as its traditional label for aggregator. These roles are even codified in laws: someone is the party who will transport (and is licensed to do so), someone else can be licensed to arrange the transport, someone else may be licensed to clear customs. If you are an aggregator, it’s you who takes that activity and its inherent risks, however you accomplish it is a secondary question. Platforms, meanwhile, cannot take these roles. FlexPort is an aggregator from any angle you look, while GT Nexus is a platform. And as new platforms emerge or are considered, I think most of them can be assessed from a leverage perspective quickly. Let me give a few examples.

Logistics platforms will tend to deal with one of the following business processes: transportation, warehousing, customs clearance, repackaging, installation / stocking, material movement planning, material tracking, and invoice to payment. And the parties to these processes are a mix of cargo owners (sometimes split between the buyer and the seller with ownership switching during logistics events), logistics asset owners & operators, 3rd party logistics service providers, financial institutions, government agencies, and technology providers. And given logistics is physical: local variations will matter (India vs. Europe, etc.). Each of these intersections of process and parties should immediately suggest a degree of leverage in the minds of someone experienced in this area.

Above all, a dominant theme in logistics platforms and the leverage of their members will be the degree on market concentration. In simple terms: logistics is mostly a sector of small companies with tiny market share. Half of logistics expenditures are on trucking (about $1.6 trillion USD per year out of ~$3.2 trillion for all of logistics of any kind). But the largest trucking companies are tiny, say ~$4 billion in relevant revenue. In logistics $4 billion in trucking revenue sounds huge. Its half as much money as Sony made on just PlayStation hardware last year: and they were loss-leading on those devices just to sell the much more profitable games. Bottom line: in a huge market (trucking) if there are only tiny players then it indicates that no one has found a true economy of scale advantage and that platforms likely can treat the providers as having little leverage.

There are still variations of leverage. How many trucking asset operators do you need on your platform to cover 80% of world volume? Millions. How many are needed for 80% of ocean container shipping? Less than 100. And how many are needed for 80% of parcel? Less than 10. What I think this tells us is that a platform won't be likely for parcel (the parcel providers are too powerful, they could essentially veto it and will do so). A platform is possible for ocean but will have to concede some aspects to the desires of the asset operators. And a platform for direct truck operators is less likely compared to an aggregator since they are so weak (commoditized) that any intermediary business will tend towards being less neutral and more directive.

Obviously, platforms have other sides to them: the cargo owners, the technology providers, the 3PLs, etc. Each side must be assessed as above. How many (non-asset operating) 3PLs are needed to cover 80% of the world market? I guess it is under 10k. How many Transport Management System vendors? I'd guess under 20, but per regional market that's probably under 10. This would tell me that a platform that has TMS vendors on one side would find it harder to accommodate their leverage (due to concentration) as compared to a platform that had 3PLs as a side.

Once we eliminate the edges and focus on the goldilocks zone, I think logistics platforms start to enter the fine details of optimal user experience, data models, integration formats, pricing, and so forth. For example, any ocean transport platform will need to acknowledge the leverage of the ocean shipping lines (Maersk, etc.) and build around their old and clunky systems for status messaging through EDI. Its 2022: any sane person would be building to RESTful APIs or GraphQL. Nope, one side of the platform will have the leverage to insist on using 30-year-old EDI messages. The same would occur in financial flows that touch USA banks. While New Zealand and now Europe have much more cost effective, fast, and reliable routing via SWIFT you'll be forced to bow to the leverage and support stuff that was devised in the era of paper checks. These are the quid-pro-quo of bringing powerful sector participants onboard. Good product managers or business leaders at the platform operator will assess and steer the platform accordingly.

Summarizing

It is good to learn from the consumer platform space (where many, many more success stories exist than in logistics). In those discussions you'll find this “aggregator vs. platform” debate. Instead of losing days of time sleuthing around, I'd propose to cut the debate short and say that platforms must optimize for the relative negotiating leverage of their constituents. If that power is too large, platforms may not be viable because a platform is an intermediary and the powerful won't allow an intermediation in their value chain. If the power is too low the would-be platform is drawn into simply taking a direct position, in effect capturing the role and value of the weak party while making them a commodity. In the middle is a goldilocks zone where somewhat powerful members will tolerate a platform if it concedes where needed to keep them interested. All of this is abstract. But I think this is a novel and powerful theory for platforms for two reasons:

It helps rule out platform businesses on the grounds that the members have too little or too much leverage. Instead of platform business models, these should be aggregators or simply not pursued, respectively.

In the goldilocks zone, it reminds us that we're optimizing for the leverage of the platform members as much as for the total value created or extracted.

Anyone in logistics will see the negotiating power disparities of our sector's major players. This directly leads to the viable or ideal form of intermediation, and then when pertinent on to finding what a group expects as a concession in order to play ball on a new platform. That's the thing to add to your mental toolkit if you are making, investing in, competition against, or considering joining a logistics platform.

In case you missed it, check out the first two parts of this four part series on platforms for the logistics sector:

Sources:

https://stratechery.com/2018/the-bill-gates-line/

https://stratechery.com/2018/the-moat-map/

https://stratechery.com/2015/aggregation-theory/

https://stratechery.com/2017/defining-aggregators/

https://stratechery.com/2019/a-framework-for-regulating-competition-on-the-internet/

https://stratechery.com/2019/shopify-and-the-power-of-platforms/